ACA Plans

ACA Plans

Annual/Open Enrollment

Annual/Open Enrollment

Choosing health insurance can feel overwhelming. Between unfamiliar terminology…

Annual/Open Enrollment

Annual/Open Enrollment

If you’ve ever enrolled in health insurance and noticed your coverage doesn’…

ACA Plans

ACA Plans

If you’ve ever wanted more control over your healthcare spending, 2026 brings…

Healthcare Costs

Healthcare Costs

This guide answers the most common “just married” questions so you can make…

ACA Plans

ACA Plans

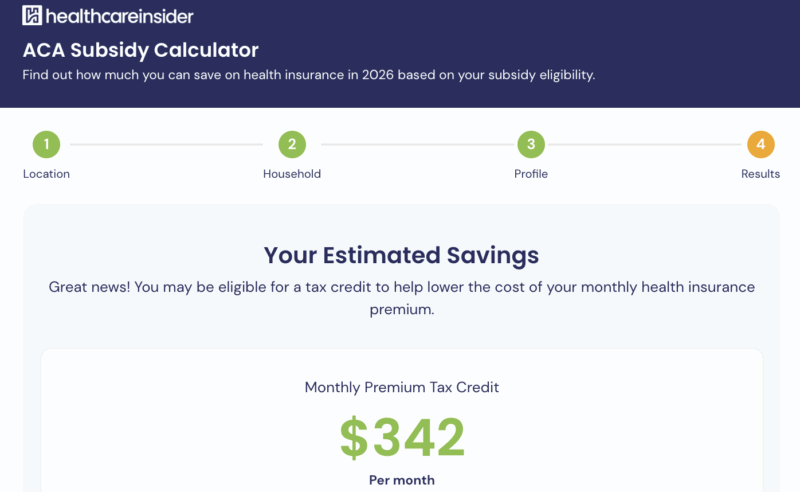

In this guide, you’ll learn how ACA subsidies work, what information you need…

Private & Alternative Health Plans

Private & Alternative Health Plans

This guide breaks down how off-market health insurance works, what types of plan…

Healthcare Costs

Healthcare Costs

How to Evaluate Mental Health Coverage Choosing the right health insurance for m…

ACA Plans

ACA Plans

How to Get Health Insurance Immediately: Same-Day & Next-Day Options If you�…

Healthcare Costs

Healthcare Costs

Overview If you’re struggling with healthcare expenses, you’re not a…

Annual/Open Enrollment

Annual/Open Enrollment

Introduction Each fall, millions of Americans ask, “When is open enrollment fo…