Did you miss the Health Insurance Open Enrollment Period? You may still be elgib…

The Affordable Care Act requires that most health insurance plans include covera…

If you’ve ever wanted more control over your healthcare spending, 2026 brings…

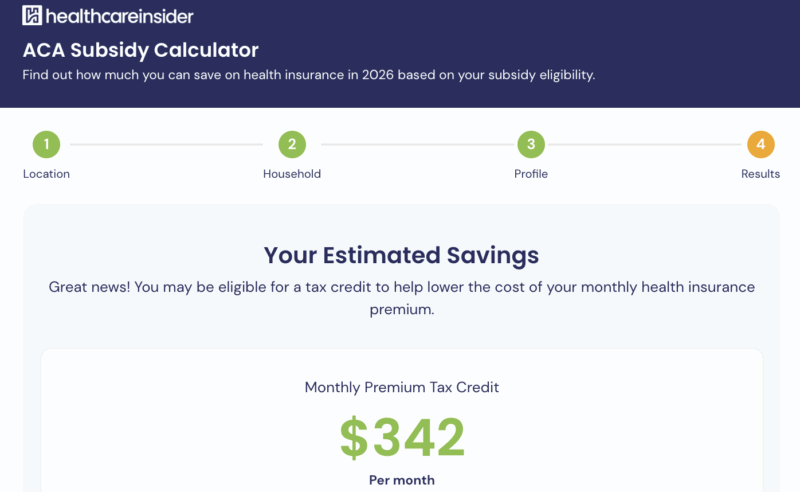

In this guide, you’ll learn how ACA subsidies work, what information you need…

How to Get Health Insurance Immediately: Same-Day & Next-Day Options If you�…

Overview Choosing the best health insurance plans for individuals can feel overw…

Overview If you’ve ever wondered whether an HSA is worth having, 2026 might be…

Understanding Your Coverage Options Before exploring age-specific guidance, it h…

Overview: A Looming Price Shock for Older ACA Enrollees Imagine turning 60 and p…

Why Are Health Insurance Premiums Going Up? If your monthly health insurance pre…

As enhanced Affordable Care Act (ACA) subsidies are set to expire, millions of A…

Overview: Why Are ACA Premiums Rising So Much? If you opened your Marketplace re…