Written by Michael LaPick

Healthcare Writer

We want to help you make educated healthcare decisions. While this post may have links to lead generation forms, this won’t influence our writing. We adhere to strict editorial standards to provide the most accurate and unbiased information.

Did you miss the Health Insurance Open Enrollment Period? You may still be elgibile to shop for plans outside this period if you have a Qualifying Life Event (QLE). Learn more below.

Overview

With the election of President Trump, many Americans have questioned the future of their Affordable Care Act (ACA), or Obamacare, health insurance plans.

Yes, ACA Marketplace plans remain in full effect. While political changes may signal potential reforms, significant shifts in health policy take time to implement, often requiring congressional approval and transition periods.

Launched in 2008 to improve health insurance access, the Affordable Care Act created Marketplaces where U.S. citizens and legal immigrants can buy coverage, often with income-based subsidies.

ACA Plan Key Features

- Marketplace Plans: Compare options on HealthCare.gov or state Marketplaces.

- Pre-existing Conditions: Coverage can’t be denied.

- Subsidies: Tax credits lower monthly premiums for eligible individuals.

Who Qualifies?

- U.S. citizens and legal immigrants without coverage from jobs, Medicare, Medicaid, or CHIP.

- Those turning 26, self-employed, unemployed, or lacking job-based coverage can explore affordable plans.

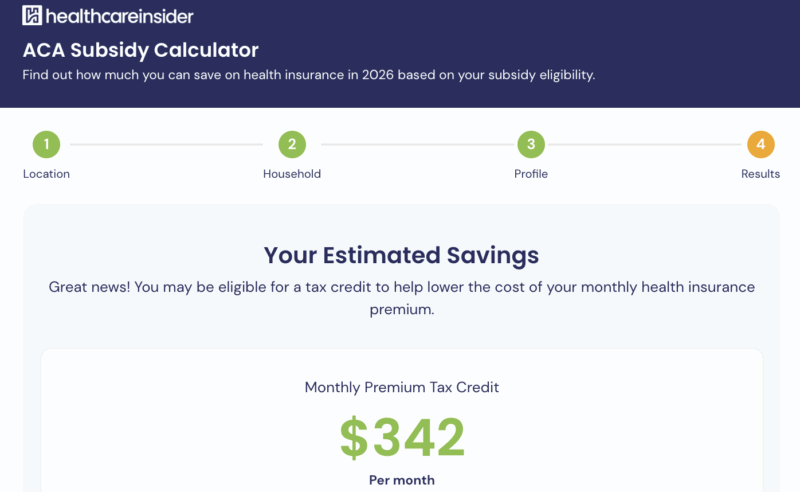

How to Save with ACA Subsidies

- Subsidies, including Premium Tax Credits (PTC), can reduce monthly premiums.

- With the Trump Administration’s recent expiration of the Inflation Reduction Act, it is projected that in 2026, individuals with household incomes between 100% and 400% of the Federal Poverty Level (FPL) will generally qualify for ACA subsidies in the form of Premium Tax Credits.

- Check your eligibility using our ACA Subsidy Calculator, regardless of your income, to see your subsidy rate or consider switching plans.

Essential Health Benefits

ACA plans cover:

- Doctor visits, emergency care, hospitalization, maternity care, mental health services, prescriptions, preventive care, and more. Before the ACA, many critical services like mental health or maternity care were often excluded.

Enrollment Periods

- Open Enrollment: Nov 1–Jan 15. Enroll by Dec 15 for Jan 1 coverage, or by Jan 15 for Feb 1 coverage.

- Special Enrollment: If you experience a Qualifying Life Event (QLE) like marriage, divorce, having a baby, losing coverage, or moving, you get a 60-day enrollment window or change plans.

A team of licensed insurance agents are here to help you compare plans

Health Insurance QLEs include:

- Changes in Household Size

- You get married;

- Pick a plan by the last day of the month and your coverage can start the first day of the next month.

- You get divorced or legally separated and lose health insurance.

- Divorce or legal separation without losing coverage doesn’t qualify you for a Special Enrollment Period.

- You have a baby, adopt a child, or place one in foster care.

- Your coverage can start the day of the event — even if you enroll in the plan up to 60 days afterward.

- The death of an individual living in your home reduces your reported household size;

- You experience a change in household size that impacts what you report to the government for your household tax subsidy.

- You get married;

- Income or Financial Changes

- You have a change in income (either an increase or decrease) and need to report it to adjust your tax subsidy

- You have an increase in income and no longer qualify for Medicaid.

- Loss of Health Coverage

- You lose your employer health insurance coverage.

- Your health insurance plan cancels your coverage, even though you’ve paid your premiums;

- Your COBRA coverage expires.

- You turn 26 years old and can no longer stay on your parent’s healthcare plan.

- Changes in Residency or Legal Status

- You move to a different ZIP code.

- You are released from jail.

- You are discharged from the Armed Forces.

- Move to the U.S. from a foreign country or United States territory.

- Or, move to or from the:

- Place you attend school (if you’re a student)

- Place you both live and work (if you’re a seasonal worker)

- Shelter or other transitional housing

- Other Special Circumstances

- You experience domestic abuse;

- When applying for health insurance, an error is made – either human or technical error – which results in you not obtaining coverage.

- Gaining membership in a federally recognized tribe or status as an Alaska Native Claims Settlement Act (ANCSA) Corporation shareholder.

- Becoming a U.S. citizen.

- Starting or ending service as an AmeriCorps State and National, VISTA, or National Civilian Community Corps (NCCC) member.

- Being affected by an unexpected and uncontrollable event or natural disaster (like an earthquake, massive flooding, or a hurricane).

ACA and Legal Challenges

The ACA has been challenged in court numerous times since it was signed into law in 2010. Below are some significant cases where the ACA was examined:

1. National Federation of Independent Business v. Sebelius (2012)

- Issue: The case challenged the constitutionality of the ACA’s individual mandate, which required most Americans to have health insurance or pay a penalty, as well as the provision that required states to expand Medicaid.

- Outcome: The Supreme Court upheld the individual mandate as a valid exercise of Congress’s taxing power. However, it struck down the provision that required states to expand Medicaid, ruling that it was coercive to threaten existing Medicaid funding for noncompliance. States were allowed to opt out of Medicaid expansion without penalty.

- Read more: Supreme Court Opinion (PDF)

2. King v. Burwell (2015)

- Issue: This case addressed whether the ACA allowed the federal government to provide subsidies to individuals in states that used federally-facilitated health insurance exchanges instead of state-run exchanges.

- Outcome: The Supreme Court ruled in a 6-3 decision that subsidies were legal nationwide, ensuring affordable health insurance coverage for individuals in all states, regardless of whether they used state or federal exchanges.

- Read more: Supreme Court Opinion (PDF)

3. Burwell v. Hobby Lobby (2014)

- Issue: The case questioned whether the ACA’s contraceptive mandate violated the religious freedoms of closely held for-profit corporations that objected to providing certain contraceptives as part of their employee health plans.

- Outcome: The Supreme Court ruled that closely held for-profit corporations could be exempt from the contraceptive mandate if they had sincere religious objections, citing protections under the Religious Freedom Restoration Act.

- Read more: Supreme Court Opinion (PDF)

4. California v. Texas (2021)

- Issue: The case challenged the constitutionality of the ACA after the individual mandate penalty was reduced to $0 by the Tax Cuts and Jobs Act of 2017, with plaintiffs arguing that the mandate’s removal rendered the entire law invalid.

- Outcome: The Supreme Court ruled in a 7-2 decision that the plaintiffs lacked standing to bring the case, effectively leaving the ACA intact.

- Read more: Supreme Court Opinion (PDF)

5. Ongoing and Lower-Court Challenges

- Issue: Numerous other legal challenges to the ACA have arisen over the years, including those targeting Medicaid expansion, contraceptive coverage rules, and employer mandates. Each challenge addressed specific provisions or interpretations of the ACA.

- Outcome: These challenges have been addressed in various courts, with many provisions of the ACA ultimately upheld.

- Read more: United States Courts – Search Opinions and Orders

Visual History of Health Insurance

Our team at Healthcare.com created this Visual History of Health Insurance in America, highlighting key events since 1972 that shaped public, private, and uninsured coverage trends.

Learn about ten key events that transformed America’s health insurance landscape and continue to inform today’s policy debates. Explore our data study.

Thank you for your feedback!